A 403(b) retirement plan is a tax-advantaged savings program available to employees of public schools, certain non-profit organizations, and employees of hospitals.

Similar to a 401(k) plan, the 403(b) allows employees to contribute pre-tax(traditional) or after-tax (Roth) to save money for retirement.

You can contribute to any of them or collectively.

For example, the 403(b) contribution limit for 2026 is $24500. So, you can add $12000 in Pre-Tax and $12500 in Roth.

But, you cannot exceed the maximum contribution limit. It is not allowed by the IRS to add $24500 to Pre-tax and even a dollar to Roth 403(b).

In simple words, collectively $24500 is ok, but $24501 is not allowed. In that case you could face tax confusion and penalties.

The IRS adjusts these limits annually based on inflation, and recent legislation, particularly the SECURE 2.0 Act, has introduced new catch-up provisions that benefit certain age groups.

For example, If you’re age 50 to 59 or 64 and older, you’re eligible for an additional $8,000 or more in catch-up contributions.

This guide will help you know everything about 403(b) contribution limits for 2024, 2025, and 2026.

403(b) Standard Contribution Limits

The standard employee contribution limit applies to most participants under age 50 are:

- $23,000 in 2024

- $23,500 in 2025

- $24,500 in 2026

These limits represent the maximum amount you can contribute through salary deferrals to your 403(b) account in a single year. This applies to both traditional (pre-tax) and Roth (after-tax) contributions combined. If you have both types of accounts, your total contributions across all 403(b) accounts cannot exceed these limits.

Total Combined Employee + Employer Contribution Limits

There is a maximum total amount that can go into your 403(b) each year. This total includes your contributions + your employer’s contributions.

- $69,000 in 2024

- $70,000 in 2025

- $72,000 in 2026

However, you cannot put in more than you actually earn from that job in the year.

You cannot put more money into your 403(b) than you earn from that job in a year. The maximum allowed is whichever is smaller: the IRS limit for that year or your total salary from that employer.

All money going into the account counts toward this limit, including the money you contribute from your paycheck, any employer matching contributions, and any additional employer contributions. There is one total cap on all the money combined.

Catch-Up Contributions to 403(b) Plan

Some employees having a 403(b) plan are eligible for additional contributions.

Standard Catch-Up (Age 50+)

Employees who are age 50 or older by the end of the calendar year are eligible for additional catch-up contributions:

- $7,500 in 2024

- $7,500 in 2025

- $8,000 in 2026

This allows older workers to grow their retirement savings as they approach retirement age. With the standard catch-up, employees aged 50+ can contribute beyond the standard limit.

- $30,500 total ($23,000 + $7,500) in 2024

- $31,000 total ($23,500 + $7,500) in 2025

- $32,500 total ($24,500 + $8,000) in 2026

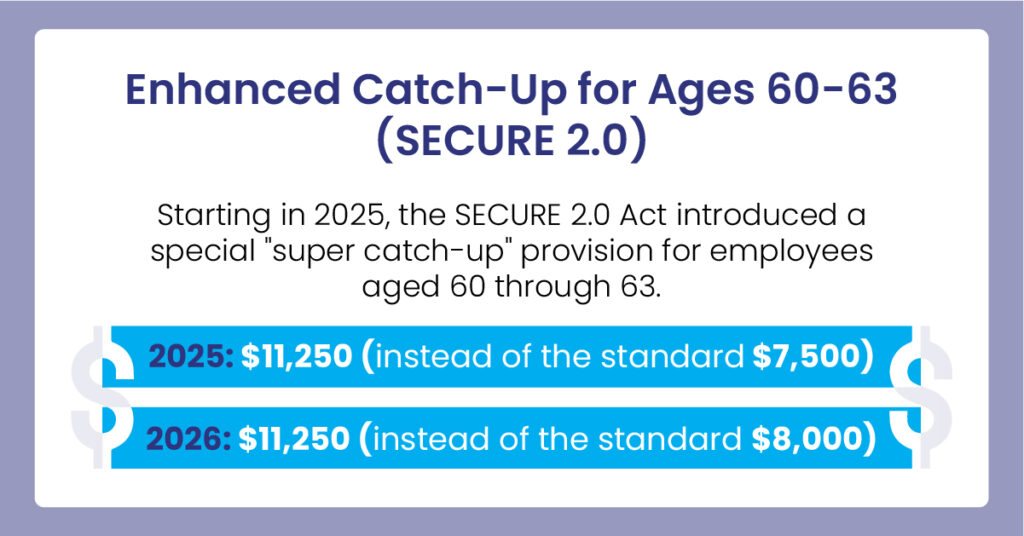

Enhanced Catch-Up for Ages 60 to 63 (SECURE 2.0)

Starting in 2025, the SECURE 2.0 Act introduced a special “super catch-up” provision for employees aged 60 through 63. This enhanced catch-up allows significantly higher contributions for this age group:

- $11,250 (instead of the standard $7,500) in 2025

- $11,250 (instead of the standard $8,000) in 2026

Employees in this age bracket can use either the age 50+ catch-up OR the enhanced 60-63 catch-up, but not both. The enhanced catch-up is the better option as it allows for higher contributions.

With the enhanced catch-up, employees aged 60-63 can contribute:

- 2025: $34,750 total ($23,500 + $11,250)

- 2026: $35,750 total ($24,500 + $11,250)

Note: This enhanced catch-up provision must be adopted by your plan. Not all 403(b) plans may offer this option immediately, so check with your plan administrator to confirm availability.

403(b) Special Catch-Up Contribution Provision for Long-Tenured Employees (15 Years)

The 403(b) plan offers a unique catch-up provision that’s not available in 401(k) plans, 15-year service catch-up. This 15-year service catch-up provision applies to employees who have completed at least 15 years of service with the same eligible employer i.e. educational institutions, hospitals, or certain other non-profit organizations.

➜ How the Special Catch-Up Plan Works

Eligible employees can contribute an additional amount, calculated as the lesser of:

- $3,000 per year until reach to $15,000 lifetime maximum

In simple words, the 15-year 403(b) catch-up lets long-term employees add up to $3,000 extra per year, capped at $15,000 total, but only if their past contributions were low enough, $75,000 or below.

Let’s make it clear from the examples:

Example 1: Employee with lower contributions than $75000

- Years worked: 15

- $5,000 × 15 = $75,000

- Total contributed so far: $50,000

➜ $75,000 − $50,000 = $25,000 available

But:

- Yearly cap = $3,000

- Lifetime cap = $15,000

As the available balance is more than $15000 so the employee is eligible for 15 years tenure 403(b) plan. That employee can contribute as special catch-up only $3000 per year, and total $15000. Contributing depends on employees whether they reach the total 5 years or more, but not less than 5 years as they cannot contribute more than 3000 dollars per year.

Example 2: Employee who already contributed a lot

- Years worked: 15

- $5,000 × 15 = $75,000

- Total contributed so far: $80,000

➜ $75,000 − $80,000 = -$5000

The employee has already contributed more than the allowed amount of $75,000, so they are not allowed special catch-up , even though they worked 15 years.

➜ Important Rules

- You can use the 15-year service catch-up together with the age 50+ catch-up if you qualify for both.

- If you are eligible for both and your plan allow, any extra money above the normal $24,500 limit goes first to the 15-year catch-up (up to its $3,000/year and $15,000 lifetime limit), and any remaining extra goes to the age 50+ catch-up.

➜ Maximum Contribution with 15-Year Catch-Up

If fully utilizing the 15-year catch-up along with standard contributions:

- Up to $26,000 ($23,000 + $3,000) in 2024

- Up to $26,500 ($23,500 + $3,000) in 2025

- Up to $27,500 ($24,500 + $3,000) in 2026

If combining with age-based catch-ups (50+), the total could reach:

- Up to $33,500 ($23,000 + $3,000 + $7,500) in 2024

- Up to $34,000 ($23,500 + $3,000 + $7,500) in 2025

- Up to $35,500 ($24,500 + $3,000 + $8,000) in 2026

For ages 60-63 with the enhanced catch-up:

- Up to $37,750 ($23,500 + $3,000 + $11,250) in 2025

- Up to $38,750 ($24,500 + $3,000 + $11,250) in 2026

403(b) Max Contribution Limits Tables

These tables will give you a clear picture of 403b maximum contribution limits.

Employee Contribution Limits ($)

| Employee Category | Year 2024 | Year 2025 | Year 2026 |

| Basic Employee Deferral Limit | $23,000 | $23,500 | $24,500 |

| Standard Catch-Up (50-59 and 64+) | $7,500 | $7,500 | $8,000 |

| Enhanced Catch-Up (Age 60-63) | N/A | $11,250 | $11,250 |

| 15-Year Service Catch-Up | $3,000/year | $3,000/year | $3,000/year |

Total Contribution Scenarios (Employees Only)

| Employee Category | Year 2024 | Year 2025 | Year 2026 |

| Under Age 50 | $23,000 | $23,500 | $24,500 |

| Ages 50-59 | $30,500 | $31,000 | $32,500 |

| Ages 60-63 (Enhanced) | N/A | $34,750 | $35,750 |

| Age 64+ | $30,500 | $31,000 | $32,500 |

| With 15-Year Service (Under 50) | Up to $26,000 | Up to $26,500 | Up to $27,500 |

| With 15-Year Service (Ages 50-59) | Up to $33,500 | Up to $34,000 | Up to $35,500 |

| With 15-Year Service (Ages 60-63) | N/A | Up to $37,750 | Up to $38,750 |

| With 15-Year Service (Age 64+) | Up to $33,500 | Up to $34,000 | Up to $35,500 |

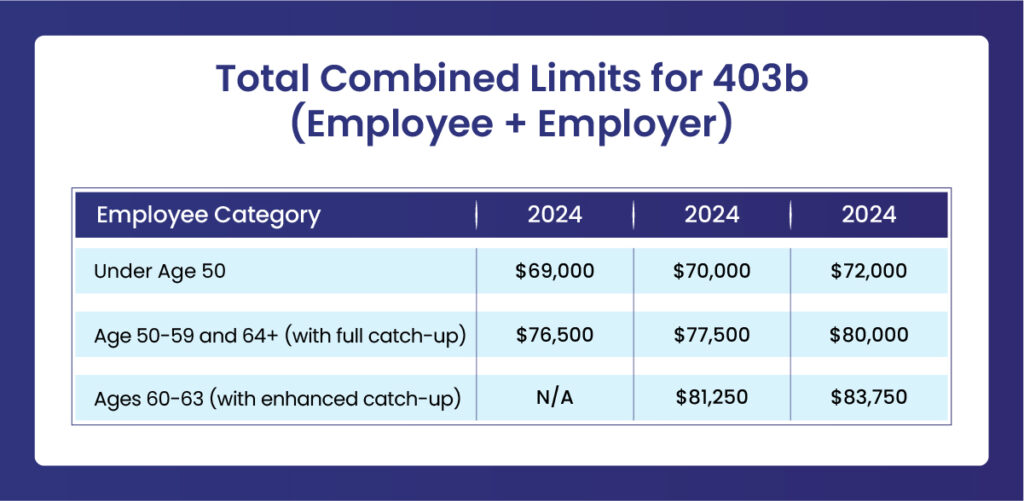

Total Combined Limits for 403b (Employee + Employer)

| Employee Category | Year 2024 | Year 2025 | Year 2026 |

| Under Age 50 | $69,000 | $70,000 | $72,000 |

| Age 50-59 and 64+ (with full catch-up) | $76,500 | $77,500 | $80,000 |

| Ages 60-63 (with enhanced catch-up) | N/A | $81,250 | $83,750 |

Important Rules and Considerations

Multiple Plans

If you participate in multiple 403(b) plans or both a 403(b) and 401(k) plan in the same year:

- The basic employee deferral limit applies to your combined contributions across all such plans

- Each employer can still make contributions up to the total combined limit for that specific plan

Example: If you contribute $23,500 to a 403(b) in 2025, you cannot also contribute to a 401(k) in the same year (unless you’re using catch-up provisions)

Roth vs. Traditional

- The contribution limits apply equally to traditional (pre-tax) and Roth (after-tax) 403(b) contributions

- You can split your contributions between both types, but the total cannot exceed the annual limit

- Employer contributions are always made on a pre-tax basis

- Roth contributions grow tax-free and can be withdrawn tax-free in retirement (subject to five-year rule and age requirements)

Timing of Contributions

- Contributions must be made during the calendar year (January 1 – December 31)

- Unlike IRAs, there’s no grace period to make prior-year contributions in the following year

- Set up your payroll deductions early in the year to maximize the benefits of dollar-cost averaging and compound growth

After-Tax Contributions

Some 403(b) plans allow after-tax (non-Roth) contributions beyond the elective deferral limit, up to the total combined limit of $69,000/$70,000/$72,000 in years 2024, 2025, and 2026 respectively. These are different from Roth contributions and have different tax treatment. Check with your plan admin about availability.

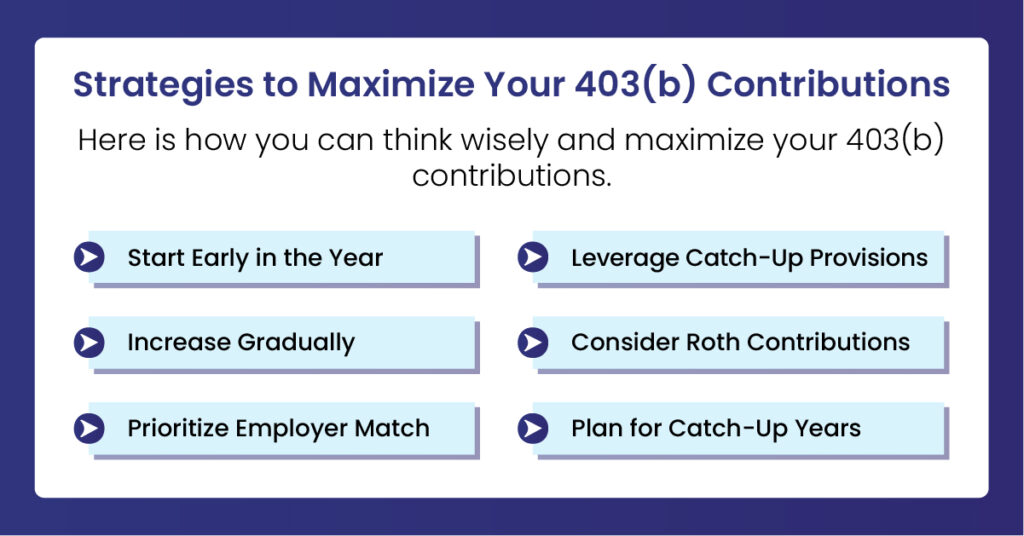

Strategies to Maximize Your 403(b) Contributions

Here is how you can think wisely and maximize your 403(b) contributions.

✔️ Start Early in the Year

Begin contributing at the start of the year to get the most out of your money. This helps spread out contributions, benefits from compound growth, and avoids last-minute scrambling to hit your limit.

✔️ Increase Gradually

If maxing out isn’t possible immediately, raise your contribution a little each year or when you get a raise. Even small increases over time can grow significantly with compounding.

✔️ Prioritize Employer Match

Always contribute enough to get your full employer match. It’s free money. Missing the match is like leaving part of your paycheck on the table.

✔️ Leverage Catch-Up Provisions

If eligible, use age-based catch-ups at 50+, the enhanced 60–63 catch-up, or the 15-year service catch-up. These let you save extra in the years you need it most.

✔️ Consider Roth Contributions

Think about whether Roth contributions make sense for your situation. Younger employees benefit from tax-free growth, while higher earners may prefer traditional pre-tax contributions. A mix can give tax diversification in retirement.

✔️ Plan for Catch-Up Years

If you’re approaching 50, 60, or have 15 years of service, plan your budget to take full advantage of catch-ups. These opportunities are limited to certain ages or years of service, so timing matters.

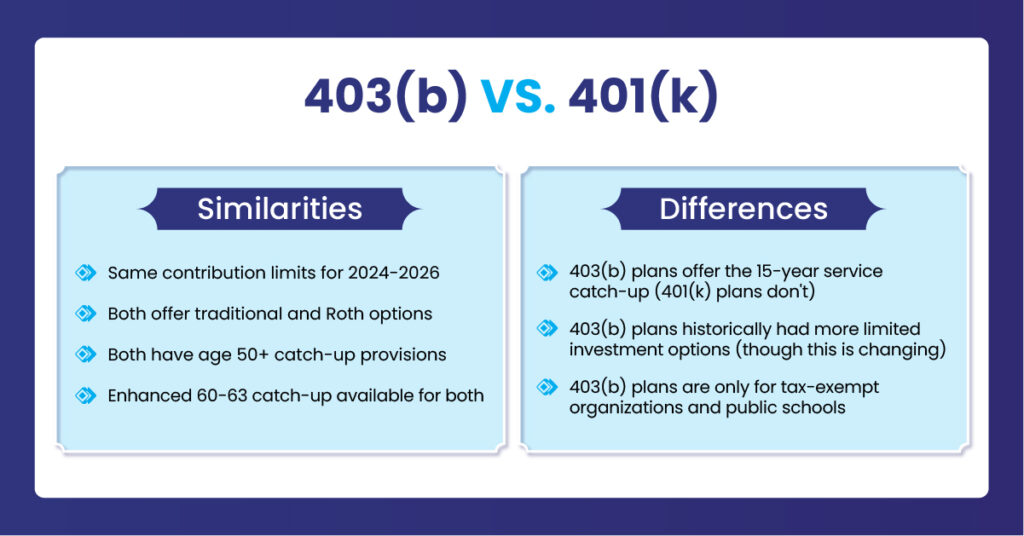

Comparing 403(b) to 401(k)

| Feature | 403(b) | 401(k) |

| Who it’s for | Employees of public schools and many tax-exempt (nonprofit) organizations | Most common at for-profit/private employers (and some other employer types) |

| Contribution limits (2024–2026) | Same IRS limits as a 401(k) | Same IRS limits as a 403(b) |

| Traditional vs. Roth | Often offers Traditional (pre-tax) and/or Roth (after-tax) | Often offers Traditional (pre-tax) and/or Roth (after-tax) |

| Age 50+ catch-up | Yes (if the plan allows it) | Yes (if the plan allows it) |

| Enhanced catch-up (ages 60–63) | Available for both plan types (if offered) | Available for both plan types (if offered) |

| Special catch-up option | May offer 15-year service catch-up (unique to 403(b)s, if you qualify) | Not available |

| Investment options (typical) | Historically more limited (often annuities), but many plans now offer strong mutual fund lineups | Often broader fund menus, but varies by employer/plan |

| Bottom line | Usually very similar to a 401(k), with the 15-year service catch-up as the standout difference | Usually very similar to a 403(b), minus the 15-year service catch-up |

While there is an important technical distinction between 403(b) plans and 401(k) plans that applies to most employees, they generally operate in a similar way. Both types of plans have the same $23,000 to $24,500 contribution limit for 2024–2026 and will typically provide traditional and Roth contributions and the typical age 50+ catch-up contribution.

Where a 403(b) can differ from a 401(k) is the 15-year service catch-up contribution. This contribution is not allowed in 401(k) plans and could potentially allow certain long tenured employees of qualifying employers to make additional contributions. It is not universally available within all 403(b) plans and the rules surrounding it are somewhat complex. Therefore, if this is available to you, you should contact the Human Resources department or the plan administrator to confirm.

Another aspect that employees tend to observe when comparing their respective plans is the investment menu. Historically, 403(b) plans have provided less investment choice and some have been focused on annuity products, however, many have moved away from this approach. The best course of action would be to review the costs and investment options within your specific plan as the quality of offerings vary greatly among both 403(b) and 401(k) plans.

Lastly, the type of plan is often reflective of the employer. 403(b) plans are primarily offered by public schools and certain tax-exempt organizations, whereas 401(k) plans are most prevalent in the private, for profit sector.

403(b) and IRA Contributions

You can contribute to both a 403(b) and an IRA in the same year:

- 403(b) limits don’t affect your ability to contribute to an IRA

- IRA limits: $7,000 (2025) and $7,500 (2026), plus $1,000/$1,100 catch-up for age 50+

- However, having a 403(b) may affect the deductibility of traditional IRA contributions depending on your income

- Roth IRA contributions are subject to income phaseouts

Employer Contributions to 403(b) Plans

Understanding how employer contributions work can significantly impact your retirement planning strategy. Your employers contribute to your 403b plan in different ways.

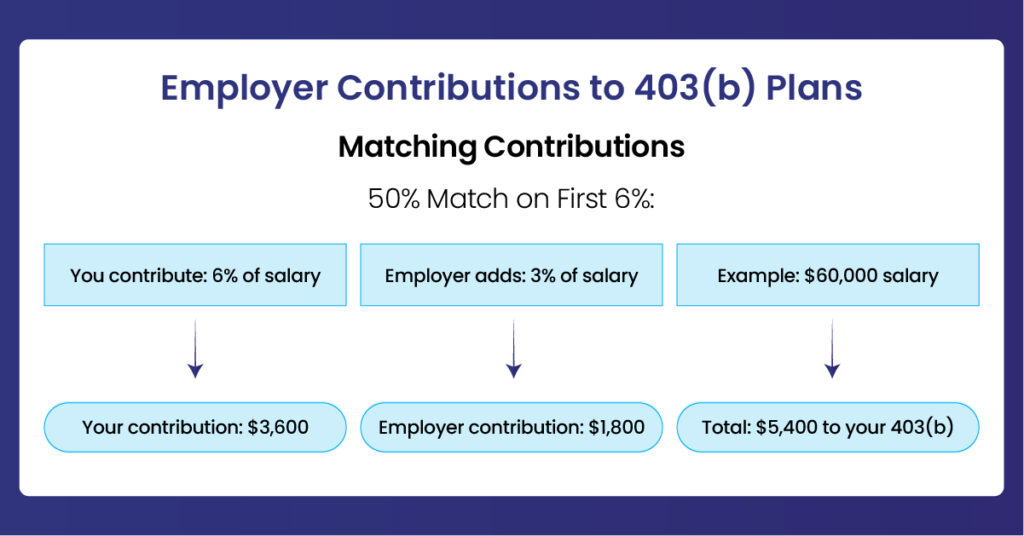

“Matching Contributions” is the most common type of employer contribution. An employer match means: you put money in, and your employer adds extra money based on what you contributed. The more you contribute (up to a limit), the more you may get from your employer.

Here are two common matching setups:

1). “50% match on the first 6% you contribute”

This means your employer gives you 50 cents for every $1 you contribute, but only on the first 6% of your pay.

Example (salary: $60,000):

- If you contribute 6%, that’s $3,600 per year.

- Your employer matches half of that (3% of salary), which is $1,800 per year.

- Total going into your 403(b) is $5,400 per year.

2). “Dollar-for-dollar match up to 3%”

This means your employer matches $1 for every $1 you contribute, but only up to 3% of your pay.

Example (salary: $60,000):

- If you contribute 3%, that’s $1,800 per year.

- Your employer contributes the same amount: $1,800 per year.

- Total going into your 403(b) is $3,600 per year.

When Employees Can Withdraw 403(b) Contributions

The majority of a 403(b) plan is intended for long term retirement savings and therefore, there are restrictions on when you will be able to withdraw money from your account.

Below we have outlined the most typical reasons when you may be able to make a withdrawal along with tax implications as well as potential penalties associated with those same withdrawals.

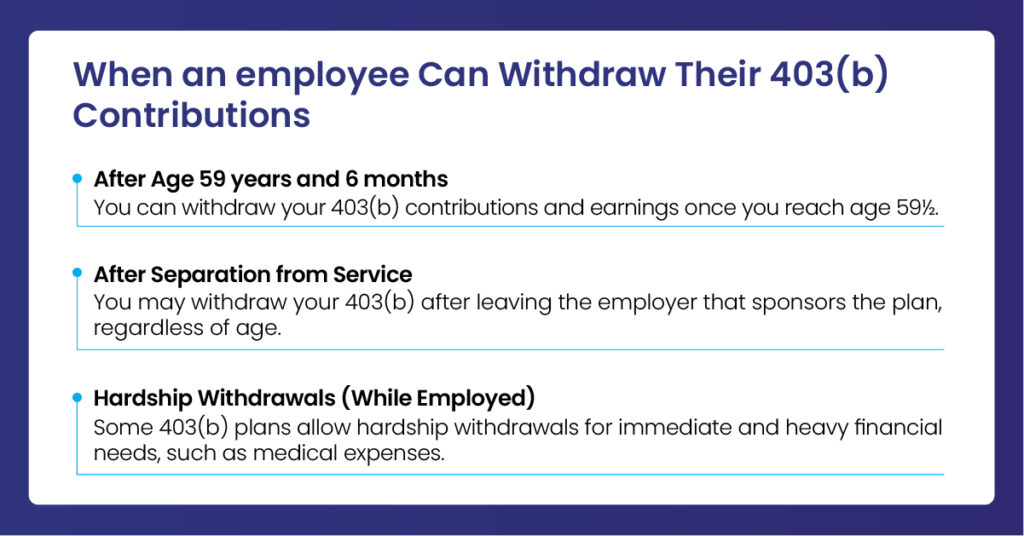

1). After Age 59½

You can withdraw your 403(b) contributions and earnings once you reach age 59½. These withdrawals are not subject to the 10% early-withdrawal penalty. Pre-tax contributions are taxable as ordinary income, while qualified Roth 403(b) withdrawals are tax-free if the account has been open for at least five years.

2). After Separation from Service

You may withdraw your 403(b) after leaving the employer that sponsors the plan, regardless of age. If you are under age 59½, the withdrawal is generally taxable and subject to a 10% early-withdrawal penalty. Some plans allow an exception to the penalty if you separate from service in or after the year you turn 55 (the “Rule of 55”).

3). Hardship Withdrawals (While Employed)

Some 403(b) plans allow hardship withdrawals for immediate and heavy financial needs, such as medical expenses, foreclosure or eviction prevention, funeral costs, or certain education or disaster expenses. These withdrawals usually include only your contributions, not earnings. The amount withdrawn is taxable.

FAQs

Can I contribute to both a 403(b) and 401(k) in the same year?

Yes, but your combined elective deferrals to both cannot exceed the annual limit ($23,500 in 2025, $24,500 in 2026). Each employer can still make contributions up to their respective total combined limits.

Do employer matching contributions count toward my contribution limit?

Employer contributions don’t count toward your elective deferral limit, but they do count toward the total combined limit ($70,000 in 2025, $72,000 in 2026).

Can I make both traditional and Roth contributions?

Yes, you can split contributions between both types, but your total cannot exceed the annual elective deferral limit.

Does the 15-year catch-up reset if I change employers?

No, the lifetime $15,000 maximum follows you, but you must have 15 years of service with your current employer to use it.

How much should I contribute to 403(b)?

Aim to contribute at least enough to get the full employer match—it’s free money. Ideally, save around 15–20% of your income each year, including employer contributions and other retirement accounts. Start early and increase contributions gradually to take advantage of compounding and reach your retirement goals comfortably.

What happens if I contribute too much to my 403(b)?

If you contribute too much to your 403(b), the excess is taxed twice—once in the year you contribute it and again when you withdraw it later. Most plans have safeguards, but if you switch jobs or have multiple plans, overcontributing can still happen.

If this occurs, contact your plan administrator to remove the extra amount and any earnings by April 15. The withdrawn excess and earnings are taxable and must be reported, usually on a modified W-2 or Form 1099-R when you file your taxes.